In today's digital-first business environment, cyber threats have become one of the most significant risks organizations face. From data breaches to ransomware attacks, the financial and reputational damage from cyber incidents can be devastating. This reality has fueled explosive growth in the cyber liability insurance market, which has emerged as a critical component of comprehensive business insurance strategies across industries.

Explosive Market Growth

The cyber insurance market has experienced remarkable expansion in recent years, growing at an impressive rate of 32% annually from 2017 to 2022. According to industry reports, the global cyber insurance premium doubled from 2017 to 2020 and then doubled again from 2020 to 2022. Market analysts project that the global cybersecurity insurance industry will reach $32.19 billion by 2030, growing from $16.54 billion in 2025.

This growth is driven by several factors, including the increasing digitization of businesses, rising awareness of cyber risks, and regulatory requirements that mandate certain levels of cyber protection. As organizations continue to digitalize their operations and store more sensitive data online, the demand for cyber liability insurance has skyrocketed across all business sizes and sectors.

Cyber insurance market segmentation showing growth across different sectors

Protecting Against Digital Threats

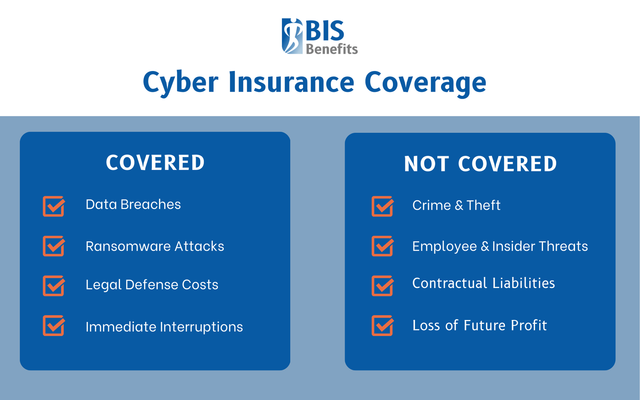

Cyber insurance provides financial protection for businesses suffering from cyberattacks and helps organizations recover from internet-based threats. Unlike traditional general liability insurance, which typically excludes cyber risks, specialized cyber policies are designed to address the unique challenges of digital incidents.

Comprehensive cyber insurance coverage typically includes first-party and third-party protections. First-party coverage helps businesses cover their own losses, including data restoration costs, business interruption losses, and cyber extortion payments. Third-party coverage protects against liability claims from customers, partners, and regulatory bodies affected by a cyber incident.

Many businesses mistakenly believe that their existing professional liability insurance or errors and omissions insurance policies adequately cover cyber risks. However, these traditional policies often have limited or no coverage for modern cyber threats, making dedicated cyber liability insurance essential for adequate protection.

Types of Cyber Insurance Coverage

The cyber insurance market offers various types of coverage tailored to different business needs:

Data Breach Coverage: Covers costs associated with data breaches, including notification expenses, credit monitoring services, and public relations efforts.

Business Interruption Coverage: Reimburses lost income and operating expenses when a cyber incident disrupts business operations.

Cyber Extortion Coverage: Provides coverage for ransomware attacks and other forms of cyber extortion, including negotiation costs and ransom payments.

Network Security Liability: Protects against claims arising from failure to prevent unauthorized access to or transmission of malware.

Privacy Liability: Covers claims related to violations of privacy rights and the mishandling of confidential information.

Regulatory Defense Coverage: Helps with costs associated with regulatory investigations and fines related to data breaches.

Understanding what cyber insurance typically covers and what it doesn't

Market Trends and Challenges

Despite its rapid growth, the cyber insurance market faces several challenges. Insurers are struggling with the increasing frequency and severity of cyber attacks, which has led to rising premiums in some segments. Additionally, the evolving nature of cyber threats makes it difficult to accurately assess and price risk.

Recent market trends indicate a shift toward more sophisticated underwriting processes, with insurers increasingly requiring businesses to implement specific cybersecurity measures as a condition of coverage. This includes requirements for multi-factor authentication, regular security assessments, and employee training programs.

Another emerging trend is the integration of cybersecurity services with insurance offerings. Some insurers now provide proactive security monitoring, threat intelligence, and incident response services as part of their cyber insurance packages, creating a more holistic approach to cyber risk management.

The Future of Cyber Insurance

Looking ahead, the cyber insurance market is expected to continue its growth trajectory, though perhaps at a more moderate pace. Industry experts predict that while cyber risks will continue to increase, improved cybersecurity practices and more sophisticated risk modeling will help stabilize the market.

Future developments in cyber insurance are likely to include AI-powered risk assessment, parametric insurance products that pay out automatically when predefined cyber risk parameters are met, and industry-specific solutions tailored to the unique risks of different sectors.

Conclusion

As digital threats continue to evolve and intensify, cyber liability insurance has become an essential component of comprehensive risk management for businesses of all sizes. The market's remarkable growth reflects both the increasing recognition of cyber risks and the need for specialized protection against digital threats.

For businesses considering cyber insurance, it's important to work with experienced brokers who understand the evolving cyber risk landscape and can help identify the most appropriate coverage. While insurance cannot prevent cyber attacks, it can provide the financial resources needed to recover from an incident and resume normal operations.

As the cyber insurance market continues to mature, we can expect more sophisticated products, better risk modeling, and closer integration between insurance and cybersecurity services—ultimately creating a more resilient digital ecosystem for businesses worldwide.