The insurance industry is undergoing a profound transformation in how risk is assessed and policies are underwritten, with artificial intelligence (AI) at the forefront of this evolution. Traditional underwriting, which relied heavily on historical data, broad demographic categories, and manual processes, is being replaced by AI-powered systems that can analyze vast amounts of data to create highly accurate, personalized risk assessments. This revolution is not just improving efficiency—it's fundamentally changing how insurance products are priced, who can access coverage, and how risks are managed across all insurance segments, from auto insurance quotes to health insurance plans.

The AI Revolution in Underwriting

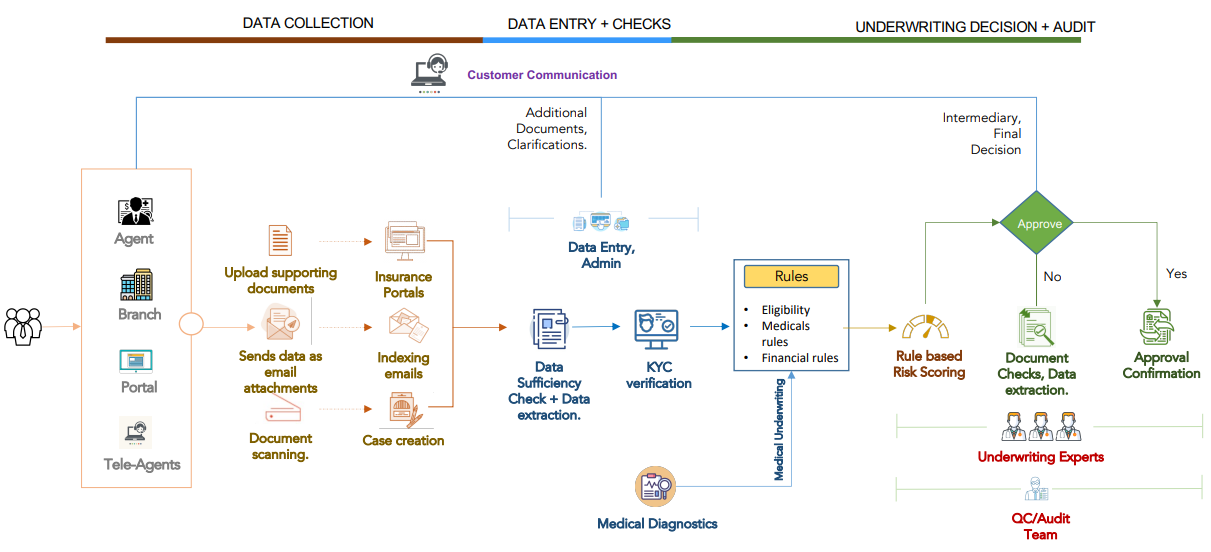

AI-powered underwriting integrates artificial intelligence into the insurance underwriting process, enabling faster, more accurate, and data-driven risk assessment. By leveraging sophisticated algorithms and machine learning models, insurers can analyze thousands of data points to uncover hidden patterns and insights that would be impossible for human underwriters to detect. This technology is transforming underwriting from a largely manual, time-consuming process into an automated, highly efficient operation that can process applications in minutes rather than days or weeks.

The impact of AI-powered underwriting extends across all insurance segments. For auto insurance quotes, AI can analyze telematics data, driving records, and even weather patterns to assess individual risk profiles with unprecedented precision. In health insurance, AI systems can process medical records, wearable device data, and genetic information (with appropriate consent) to create personalized health insurance plans that accurately reflect individual health risks.

Applications and benefits of AI in commercial insurance underwriting

Key Technologies Powering AI Underwriting

Several technologies are at the core of AI-powered underwriting:

Machine Learning: ML algorithms can analyze historical claims data to identify patterns and predict future risks, continually improving their accuracy as they process more data.

Deep Learning: A subset of machine learning that uses neural networks to analyze complex, unstructured data like images, text, and audio.

Natural Language Processing (NLP): NLP enables systems to extract relevant information from unstructured documents like medical records, accident reports, and financial statements.

Predictive Analytics: These tools use historical data to forecast future events, helping insurers anticipate potential claims and adjust pricing accordingly.

Computer Vision: This technology can analyze images and videos to assess property damage, vehicle condition, or other visual risk factors.

Applications Across Insurance Types

AI-powered underwriting is transforming risk assessment across virtually all insurance segments:

In property and casualty insurance, AI systems can analyze satellite imagery, weather data, and property characteristics to assess risk for home insurance quotes, flood insurance, and earthquake insurance. For auto insurance quotes, AI can process telematics data, driving records, and even social media activity (with consent) to create highly personalized risk profiles.

Life insurance underwriting has been revolutionized by AI, which can analyze electronic health records, wearable device data, and genetic information to provide more accurate life insurance quotes. This has enabled innovations like no medical exam life insurance and more precise pricing for term life insurance, whole life insurance, and universal life insurance.

Health insurance underwriting benefits from AI's ability to analyze vast amounts of medical data, enabling more accurate risk assessment for individual health insurance, family health insurance, and specialized plans like Medicare Advantage and short-term health insurance.

Business insurance underwriting has been transformed through AI's ability to analyze industry-specific data, financial records, and operational metrics. This applies to commercial auto insurance, general liability insurance, professional liability insurance, and workers' compensation insurance.

Even specialized insurance products like cyber liability insurance, pet insurance, and travel insurance are benefiting from AI-powered underwriting, with tailored models that address their unique risk factors.

Benefits for Insurers and Customers

AI-powered underwriting creates significant benefits for both insurers and customers:

Speed and Efficiency: What once took days or weeks can now be accomplished in minutes, dramatically reducing the time from application to policy issuance.

Accuracy: AI systems can analyze more data points and identify patterns that humans might miss, resulting in more accurate risk assessments and pricing.

Personalization: AI enables highly individualized risk assessments, allowing insurers to offer personalized coverage and pricing rather than one-size-fits-all policies.

Cost Reduction: Automated underwriting reduces the need for manual intervention, lowering operational costs for insurers.

Expanded Coverage: By accurately assessing previously uninsurable or underinsured risks, AI can help expand access to insurance coverage.

Insurance business process enhanced by AI-powered underwriting

Dynamic Risk Assessment

One of the most significant advantages of AI-powered underwriting is the ability to perform dynamic risk assessment that adapts to changing circumstances in real-time. Traditional underwriting typically assessed risk at a single point in time, with policies remaining static until renewal. AI systems, however, can continuously monitor and update risk assessments based on new data.

For example, an AI system might adjust a driver's risk profile based on recent telematics data showing improved driving habits, potentially lowering their auto insurance quotes. Similarly, a homeowner's risk profile might be updated after installing smart home devices that reduce the likelihood of fire or water damage.

This dynamic approach to risk assessment creates a more accurate reflection of actual risk, leading to fairer pricing and more appropriate coverage. It also incentivizes policyholders to engage in risk-reducing behaviors, creating a virtuous cycle of improved risk management.

Challenges and Considerations

Despite its many benefits, implementing AI-powered underwriting presents several challenges:

Data Quality and Availability: AI systems require large amounts of high-quality data to function effectively. Insurers must ensure they have access to accurate, comprehensive data from various sources.

Algorithmic Bias: AI models can inadvertently perpetuate or amplify existing biases in historical data, potentially leading to unfair or discriminatory outcomes. Insurers must carefully monitor and adjust their models to ensure fairness.

Regulatory Compliance: Insurance is heavily regulated, and AI systems must comply with all relevant regulations while maintaining transparency in decision-making.

Explainability: Complex AI models can be difficult to interpret, making it challenging to explain underwriting decisions to customers and regulators. Insurers must balance model sophistication with the need for transparency.

Integration with Legacy Systems: Many insurers operate on legacy systems that weren't designed for AI technologies, requiring significant investment in system upgrades or replacements.

The Future of AI-Powered Underwriting

As AI technologies continue to evolve, the future of underwriting will be characterized by even greater precision, personalization, and automation. We can expect to see:

Generative AI: Advanced language models will be able to generate personalized policy documents, explain complex coverage terms in plain language, and even create customized insurance products.

Predictive Underwriting: AI systems will increasingly focus on predicting future risks rather than just assessing current ones, enabling more proactive risk management.

Real-Time Underwriting: With the proliferation of IoT devices and real-time data streams, underwriting will become increasingly dynamic, with risk assessments updated continuously.

Hyper-Personalization: AI will enable truly individualized insurance products that adapt to each customer's unique circumstances and changing needs.

Conclusion

AI-powered underwriting is not just improving the efficiency of insurance operations—it's fundamentally transforming how risk is assessed, priced, and managed. By leveraging advanced technologies to analyze vast amounts of data, insurers can create more accurate, personalized, and responsive insurance products that better meet the needs of modern customers.

From umbrella insurance to wedding insurance, AI is enabling more sophisticated risk assessment across all insurance segments. The insurers who embrace this transformation, focusing on ethical implementation and human oversight alongside technological innovation, will be best positioned to thrive in the evolving insurance landscape.

As we look to the future, the line between underwriting and other insurance functions will continue to blur, creating new opportunities for innovation and value creation. The most successful insurers will be those that view AI not as a replacement for human expertise but as a powerful tool to enhance it, creating a more efficient, accurate, and inclusive insurance industry for all.