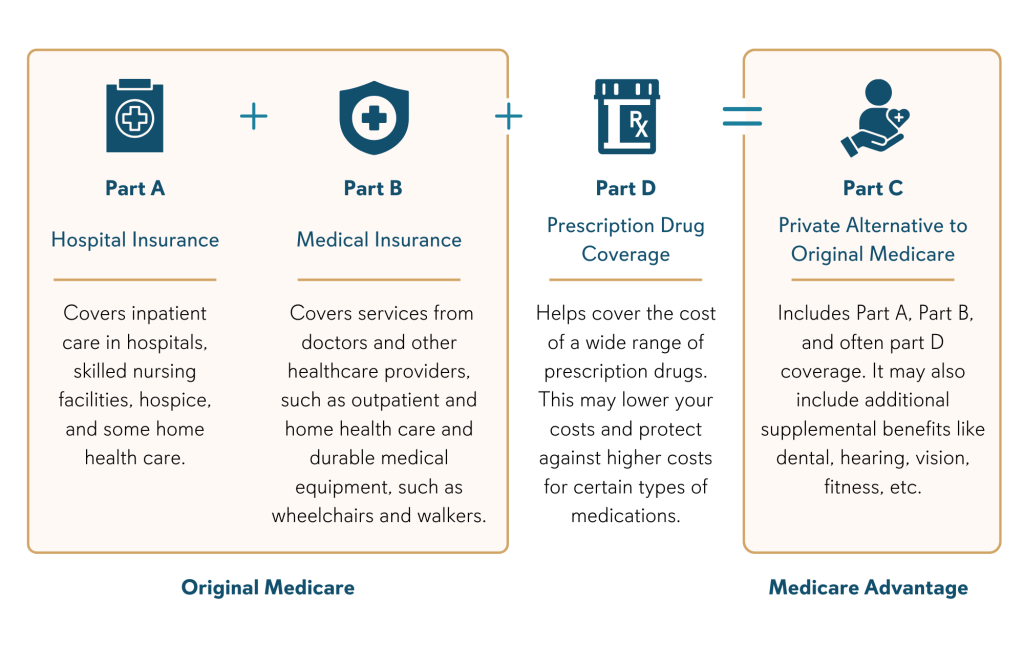

As the senior population continues to grow, Medicare Advantage plans have emerged as an increasingly popular alternative to Original Medicare. These private insurance options, also known as Medicare Part C, combine hospital (Part A) and medical (Part B) coverage, often including prescription drug coverage (Part D) and additional benefits not available through traditional Medicare. Understanding the latest trends in Medicare Advantage can help seniors make informed decisions about their healthcare coverage.

Medicare Advantage vs. Original Medicare

Before diving into trends, it's essential to understand how Medicare Advantage plans differ from Original Medicare:

Coverage Structure: Original Medicare is a fee-for-service program where you can see any doctor or hospital that accepts Medicare. In contrast, Medicare Advantage plans operate like private health insurance, typically using provider networks.

Additional Benefits: While Original Medicare covers hospital and medical services, Medicare Advantage plans often include prescription drug coverage, dental, vision, hearing, and wellness programs.

Cost Structure: Original Medicare typically requires separate premiums for Part B and Part D, plus deductibles and coinsurance. Medicare Advantage plans usually have a single premium with predictable copayments for services.

Out-of-Pocket Maximum: Original Medicare has no out-of-pocket maximum, while Medicare Advantage plans cap your annual out-of-pocket expenses.

Current Trends in Medicare Advantage

The Medicare Advantage landscape continues to evolve with several significant trends shaping the market:

Types of Medicare Advantage Plans

Several types of Medicare Advantage plans are available, each with distinct features:

Health Maintenance Organization (HMO) Plans: Typically require you to use healthcare providers within the plan's network, except in emergencies. These plans often have lower premiums and out-of-pocket costs.

Preferred Provider Organization (PPO) Plans: Offer more flexibility to see out-of-network providers, though at higher costs. These plans don't usually require referrals to see specialists.

Private Fee-for-Service (PFFS) Plans: Allow you to see any Medicare-approved provider who accepts the plan's payment terms, without requiring referrals.

Special Needs Plans (SNPs):strong> Designed for individuals with specific needs or conditions, such as chronic conditions, institutionalized individuals, or those eligible for both Medicare and Medicaid.

Medical Savings Account (MSA) Plans: Combine a high-deductible health plan with a medical savings account that the plan deposits money into for your medical expenses.

Cost Considerations

Understanding the cost structure of Medicare Advantage plans is crucial for making an informed decision:

Premiums: While you still pay your Part B premium, many Medicare Advantage plans have $0 additional premiums, though some may charge additional amounts.

Copayments and Coinsurance: Plans charge fixed amounts (copayments) or percentages (coinsurance) for services, which vary by plan and service type.

Out-of-Pocket Maximum: All Medicare Advantage plans have an annual out-of-pocket maximum, after which the plan covers 100% of covered services.

Drug Coverage: Most plans include prescription drug coverage, but formularies and costs vary significantly between plans.

Network Restrictions: Using out-of-network providers (when allowed) typically results in higher costs or no coverage at all.

Choosing the Right Medicare Advantage Plan

Selecting the appropriate Medicare Advantage plan requires careful consideration of your specific needs:

The Future of Medicare Advantage

Several emerging trends suggest how Medicare Advantage will continue to evolve:

Personalized Benefits: Plans are increasingly offering customizable benefit packages tailored to individual health needs and preferences.

Social Determinants of Health: Greater focus on addressing social factors that impact health, such as housing, nutrition, and transportation.

Artificial Intelligence: AI and machine learning are being used to identify high-risk members, predict health events, and personalize care interventions.

Expanded Telehealth: Virtual care options are likely to become even more integrated into plan benefits, potentially reducing the need for in-person visits.

Greater Integration with Supplemental Benefits: The line between medical coverage and supplemental benefits will continue to blur, with more holistic approaches to senior health.

Final Thoughts

Medicare Advantage plans have transformed from basic alternatives to Original Medicare into comprehensive healthcare solutions that address the diverse needs of today's seniors. With expanded benefits, coordinated care, and predictable costs, these plans offer compelling advantages for many beneficiaries.

When evaluating Medicare Advantage options, consider not just your current healthcare needs but also how those needs might change in the future. Look for plans that offer the right balance of coverage, cost, and convenience for your specific situation.

Remember that you can review and change your Medicare Advantage coverage annually during the Open Enrollment Period (October 15 - December 7). Take advantage of this opportunity to reassess your needs and ensure your coverage continues to meet them.

As the healthcare landscape continues to evolve, Medicare Advantage plans will likely continue to innovate and expand their offerings, providing seniors with increasingly sophisticated and personalized healthcare options. By staying informed about these trends and carefully evaluating your options, you can select a plan that provides the coverage and benefits you need to maintain your health and wellbeing in retirement.