As we age, the likelihood of needing assistance with daily activities increases. Long-term care insurance is designed to cover the costs of services that help individuals with chronic illnesses, disabilities, or other conditions that limit their ability to perform basic activities of daily living. Planning for these potential needs early can provide peace of mind and financial security for you and your loved ones.

Understanding Long-Term Care Insurance

Long-term care insurance is a type of coverage that helps pay for the cost of long-term care services when you can no longer perform basic activities of daily living (ADLs) such as bathing, dressing, eating, continence, toileting, and transferring. These services can be provided in various settings, including your home, adult day care centers, assisted living facilities, and nursing homes.

Unlike traditional health insurance or Medicare plans, which typically cover only short-term, medically necessary care, long-term care insurance is specifically designed to cover extended care that may be needed for months or years. This distinction is crucial, as many people mistakenly believe that Medicare or other health insurance will cover these long-term services, which is often not the case.

Why Long-Term Care Insurance Matters

The need for long-term care is more common than many people realize. According to the U.S. Department of Health and Human Services, someone turning 65 today has almost a 70% chance of needing some type of long-term care services in their remaining years. The costs of these services can be substantial:

- The national median cost of a private room in a nursing home is over $100,000 per year

- Assisted living facilities average around $50,000 annually

- Home health aide services cost approximately $50 per hour

Without proper planning, these expenses can quickly deplete retirement savings and force difficult financial decisions. Long-term care insurance helps protect your assets and ensures you have access to quality care when needed.

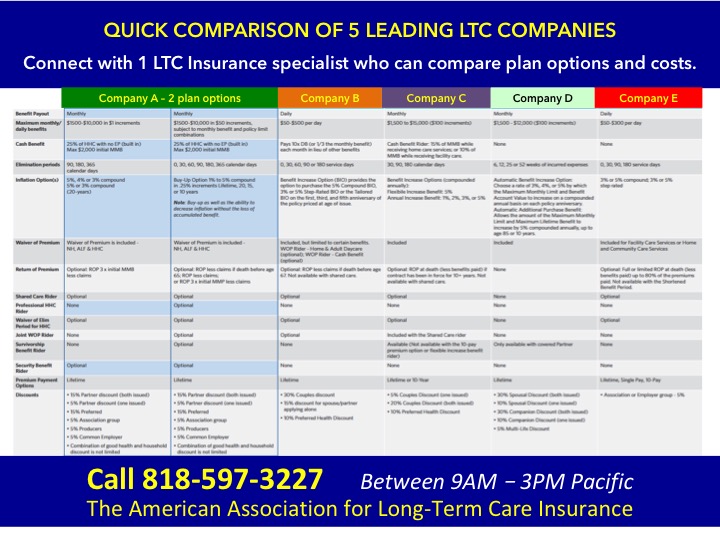

Types of Long-Term Care Coverage

When exploring long-term care insurance options, you'll encounter several types of policies:

When to Purchase Long-Term Care Insurance

The ideal time to purchase long-term care insurance is when you're healthy and still working, typically in your 50s or early 60s. Here's why timing matters:

Lower Premiums: Premiums are based on your age at the time of purchase. The younger you are when you buy a policy, the lower your premiums will be.

Better Eligibility: You're more likely to qualify for coverage when you're healthy. Pre-existing conditions can make you ineligible or result in higher premiums.

More Options: Younger applicants typically have access to a wider range of policy options and features.

Longer Accumulation: For hybrid policies, starting earlier allows more time for cash value to accumulate.

Choosing the Right Long-Term Care Policy

When selecting a long-term care insurance policy, consider these key factors:

Costs and Payment Options

The cost of long-term care insurance varies based on several factors, including your age, health status, coverage amount, benefit period, and optional features. Premiums can range from a few hundred to several thousand dollars annually.

Payment options include:

Level Premiums: Fixed premiums that remain the same throughout the life of the policy.

Limited Pay: Higher premiums for a specified period (10-20 years), after which the policy is paid up.

Single Premium: One lump-sum payment that funds the entire policy.

Some policies offer premium waivers if you become disabled or require long-term care, and some provide return-of-premium features if you never use the benefits.

Alternatives to Traditional Long-Term Care Insurance

If traditional long-term care insurance isn't right for you, consider these alternatives:

Self-Insurance: Setting aside sufficient assets to cover potential long-term care costs. This requires substantial savings and careful financial planning.

Hybrid Life Insurance Policies: Life insurance with long-term care riders that allow you to use the death benefit for care expenses while still providing a death benefit to beneficiaries.

Annuities with Long-Term Care Riders: Annuities that provide enhanced payouts if you need long-term care.

Medicaid Planning: Structuring assets to qualify for Medicaid, which does cover long-term care services but has strict eligibility requirements.

Reverse Mortgages: For homeowners, this option can provide funds to pay for care while allowing you to remain in your home.

Tips for Long-Term Care Planning

When planning for future healthcare needs, keep these tips in mind:

Final Thoughts

Planning for long-term care insurance is an essential component of comprehensive retirement planning. While it may be uncomfortable to think about potential future care needs, addressing these issues proactively can provide peace of mind and financial security for you and your loved ones.

Remember that the best long-term care strategy is one that's tailored to your specific situation, health status, financial resources, and personal preferences. By exploring your options now and making informed decisions, you can ensure you'll have access to quality care when you need it most, without compromising your financial independence or burdening your family.

Whether you choose traditional long-term care insurance, a hybrid policy, or another planning strategy, the important thing is to take action now. The future is uncertain, but with proper planning, you can face it with confidence and dignity.