What would happen if your home insurance became unaffordable or unavailable due to climate change risks in your area?

The Climate Change Insurance Crisis

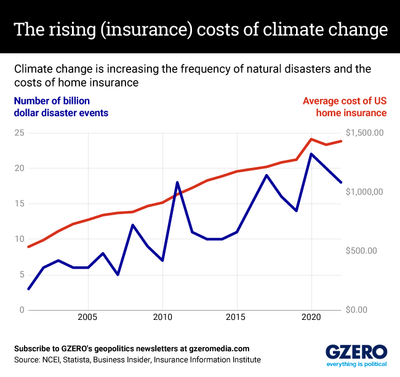

Climate change is fundamentally reshaping the home insurance quotes landscape across the globe. As extreme weather events become more frequent and severe, insurance companies are facing unprecedented losses, leading to dramatic increases in premiums and, in some cases, complete withdrawal of coverage in high-risk areas. This transformation is creating significant challenges for homeowners who suddenly find themselves paying more for less coverage or struggling to obtain insurance at all.

Climate-related disasters are causing unprecedented damage to homes worldwide

The insurance industry is responding to these climate risks by adjusting their risk models, increasing premiums, and in some cases, exiting markets entirely. According to recent data, insurers have canceled nearly two million homeowner policies in high-risk areas over a five-year period, leaving many homeowners without options for protecting their most valuable asset.

Rising Premiums Across the Board

Homeowners across the country are experiencing significant increases in their insurance premiums, with average rates jumping 24% in recent years. These increases are driven by several factors:

- Increased Frequency of Extreme Events: More frequent hurricanes, wildfires, floods, and other disasters are driving up claim costs.

- Higher Rebuilding Costs: Labor and material shortages following disasters have increased reconstruction expenses.

- Expensive Reinsurance: Insurance companies themselves are paying more for their own coverage, passing these costs to consumers.

- Improved Risk Modeling: Better climate data is revealing previously underestimated risks in many areas.

These premium increases are particularly pronounced in regions most vulnerable to climate change impacts, such as coastal areas prone to hurricanes, western states facing wildfire risks, and regions experiencing more severe flooding events.

Specialized Coverage Challenges

Certain types of climate-related risks present particular challenges for the insurance market:

- Flood Insurance: Traditional home policies typically exclude flood damage, requiring separate coverage through the National Flood Insurance Program or private insurers. As flood risks expand beyond designated flood zones, many homeowners are discovering they lack adequate protection.

- Wildfire Insurance: Insurers in western states are increasingly restricting coverage in wildfire-prone areas, with some refusing to renew policies or charging prohibitively high premiums.

- Earthquake Insurance: While not directly caused by climate change, some research suggests climate-induced stress on the Earth's crust may increase seismic activity in certain regions.

These specialized coverage gaps are particularly problematic because they often affect homeowners who may not be aware of their specific risks until it's too late. Many homeowners mistakenly believe their standard policies cover all natural disasters, only to discover significant exclusions after a catastrophic event.

Impact on Home-Based Businesses

The climate insurance crisis also affects those who operate businesses from their homes. Business insurance for home-based operations often depends on the underlying property insurance coverage. When property insurance becomes unavailable or unaffordable, it creates a domino effect that can jeopardize home-based businesses as well.

This is particularly challenging for entrepreneurs in high-risk areas who may find themselves unable to secure comprehensive business insurance coverage, potentially threatening their livelihood and the local economy.

Regional Variations in Coverage Availability

The impact of climate change on insurance availability varies significantly by region:

- Coastal Areas: Hurricane-prone regions are seeing the most dramatic premium increases and coverage restrictions.

- Western States: Wildfire risks are leading to insurance non-renewals in California, Oregon, and other western states. Flood-Prone Regions: Areas previously considered low-risk are experiencing more frequent flooding, challenging existing insurance models.

- Midwest: Increased severe weather events are driving up premiums even in traditionally stable markets.

Insurance costs are rising dramatically in areas most affected by climate change

These regional variations are creating what experts call an "insurance crisis" in certain areas, where homeowners struggle to find any coverage at reasonable rates, potentially threatening property values and local economies.

How Homeowners Can Adapt

As the insurance landscape evolves, homeowners can take several steps to protect themselves:

- Risk Mitigation: Investing in home improvements that reduce climate risks, such as fire-resistant materials, elevated foundations, or reinforced roofing.

- Comprehensive Coverage: Ensuring policies cover all relevant climate risks, including separate flood insurance where needed.

- Regular Policy Reviews: Annually reviewing coverage to ensure it keeps pace with changing risks and rebuilding costs.

- Shopping Around: Comparing options from multiple insurers, including newer companies that may use different risk models.

- Advocacy: Supporting community-level resilience efforts and policy changes that address systemic insurance challenges.

Conclusion: Navigating the New Insurance Reality

The relationship between climate change and home insurance quotes represents one of the most significant financial challenges facing homeowners today. As premiums rise and coverage becomes more restrictive, homeowners must become more proactive in understanding their risks and securing appropriate protection.

This transformation of the insurance market is likely to continue as climate impacts intensify. By staying informed, investing in resilience, and advocating for systemic solutions, homeowners can better navigate this evolving landscape and protect their homes against the uncertainties of a changing climate.